The Copper Chokepoint

The “electrify everything” mandate has run into a hole in the ground.

You cannot build a gigawatt data center, modernize a power grid, mass-produce electric vehicles, or scale a next-generation defense base without copper. It is the inescapable connective tissue of the modern economy. Yet, while the demand side of this equation is scaling at the frictionless speed of software, the supply side remains tethered to the brutal physical realities of geology, permitting delays, and heavy machinery.

Under The Cascade Thesis, this is an intersection of Graph 1 (The AI-Resource Collision), Graph 4 (The Energy Transition Paradox), and Graph 3 (Geopolitical Decoupling). The causal chain is unforgiving: exponential demand from AI, grid expansion, and defense collides with a mining sector that requires 17 years to bring a new discovery to production. The result is a structural deficit that forces a geopolitical scramble for new supply—a scramble that leads directly to the Central African Copperbelt. The market will fight this deficit with high prices, substitution, and recycling—but those forces take years to bite, and the gap they must close is enormous. That tension, not a tidy shortage, is where the opportunity lives.

The Mathematics of the Chokepoint

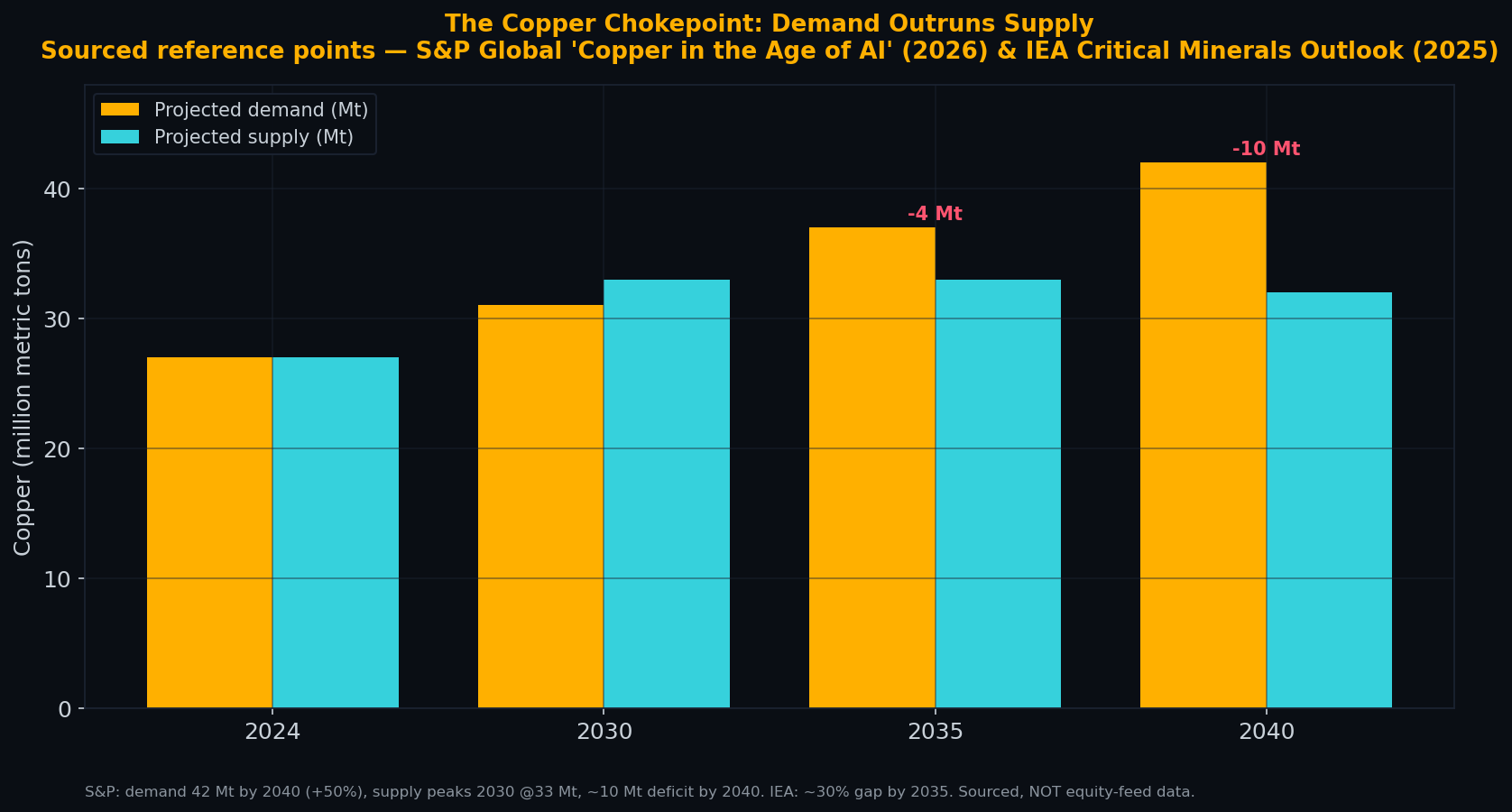

The mathematics defining this deficit are stark. According to a comprehensive 2026 study by S&P Global, the accelerating pace of electrification alone will swell global copper demand to 42 million metric tons by 2040—a staggering 50% increase from current levels [1].

Simultaneously, existing mine supply is struggling against geology itself. The average grade of mined copper ore has fallen by roughly 40% since 1991, even as nearly half of the world’s copper mines have passed the 20-year mark [1]. Richer deposits are being exhausted, and what remains is lower-grade, deeper, and more expensive to extract. The result: S&P Global projects that global copper production will actually peak in 2030 at 33 million metric tons—and decline from there.

When you subtract a declining supply curve from an exponential demand curve, you create a structural chokepoint. S&P Global projects a structural supply deficit of 10 million metric tons by 2040—a gap equal to 25% of projected demand [1]. The IEA, employing a different methodology, points to a 30% supply deficit by 2035 under current policies, which widens to a severe 40% shortfall in a net-zero scenario [2].

This gap is widening precisely because new vectors of demand are hitting the market simultaneously. The grid investment required to support the energy transition topped $390 billion in 2024 alone [3]. Meanwhile, demand from AI data centers and rising global defense spending are each expected to roughly triple by 2040 [1].

The Geopolitical Scramble and the Zambia Pivot

When the world realizes it is short 10 million tonnes of its most critical metal, the focus shifts to where new supply can actually be unearthed. This brings the Cascade Thesis directly into the realm of geopolitics.

Currently, copper processing is heavily concentrated. China commands roughly 40% of total smelting capacity and 66% of the imports of mined copper concentrate [1]. As Western nations seek to loosen this grip, they are turning to the Central African Copperbelt—and specifically to Zambia.

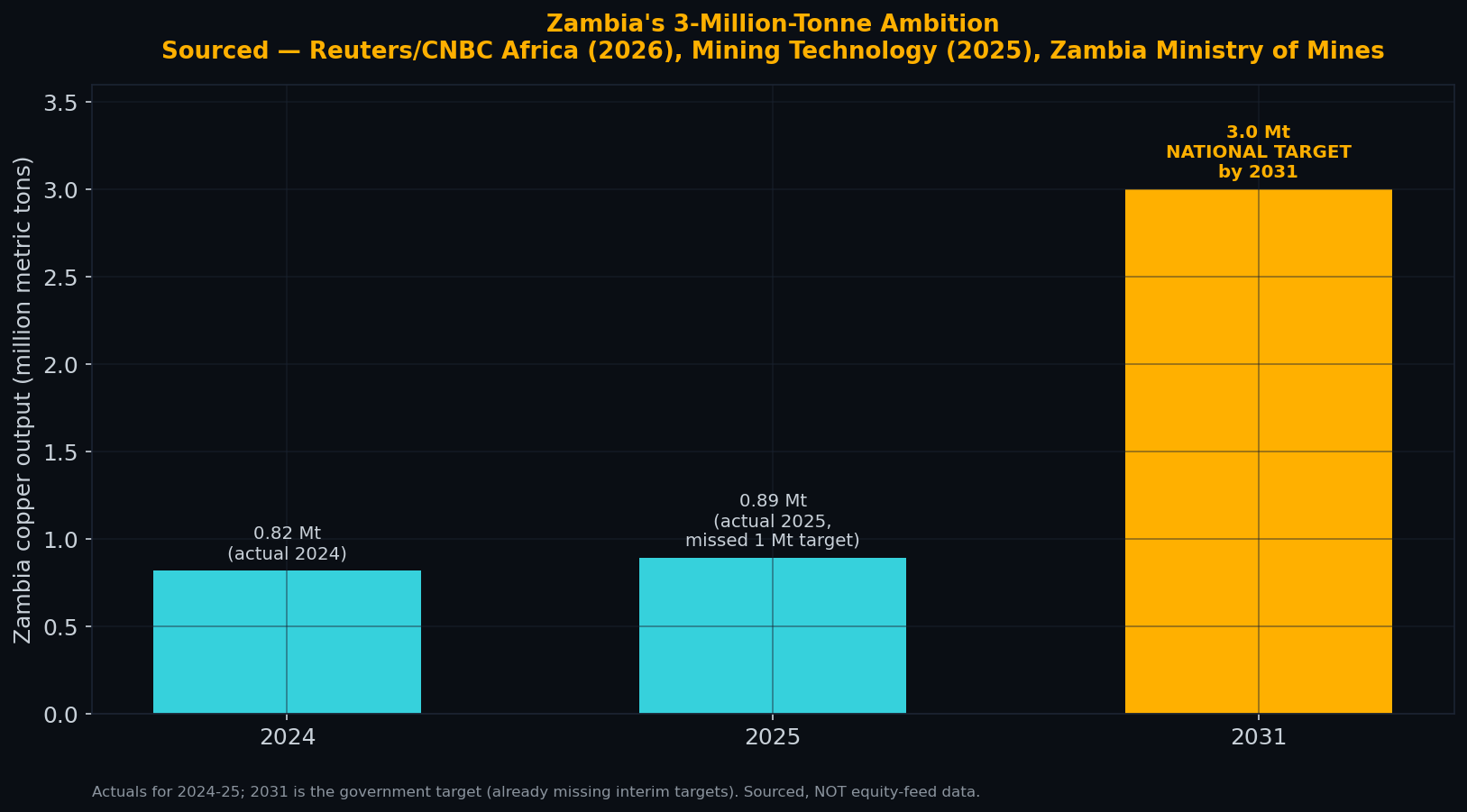

Zambia is Africa’s second-largest copper producer, accounting for roughly 3% of global output [4]. The Zambian government has recognized its strategic leverage, setting an aggressive national target to more than triple its copper output from roughly 890,000 tonnes in 2025 to 3 million tonnes annually by 2031 [5].

To make this African copper accessible to Western markets without routing it through adversarial supply chains, the United States and the European Union are backing the Lobito Corridor—a railway project connecting the mineral-rich regions of the Democratic Republic of Congo and northwestern Zambia directly to the Atlantic port of Lobito in Angola [6].

This is Graph 3 (Geopolitical Decoupling) in physical form: billions of dollars in infrastructure being laid down to secure a friendly supply line for the metal that makes AI and electrification possible.

The Investable Nodes

The terminal nodes of this cascade are the entities that control the copper in the ground. The market has begun to reprice these assets, but the expression of this trade requires navigating severe cyclicality.

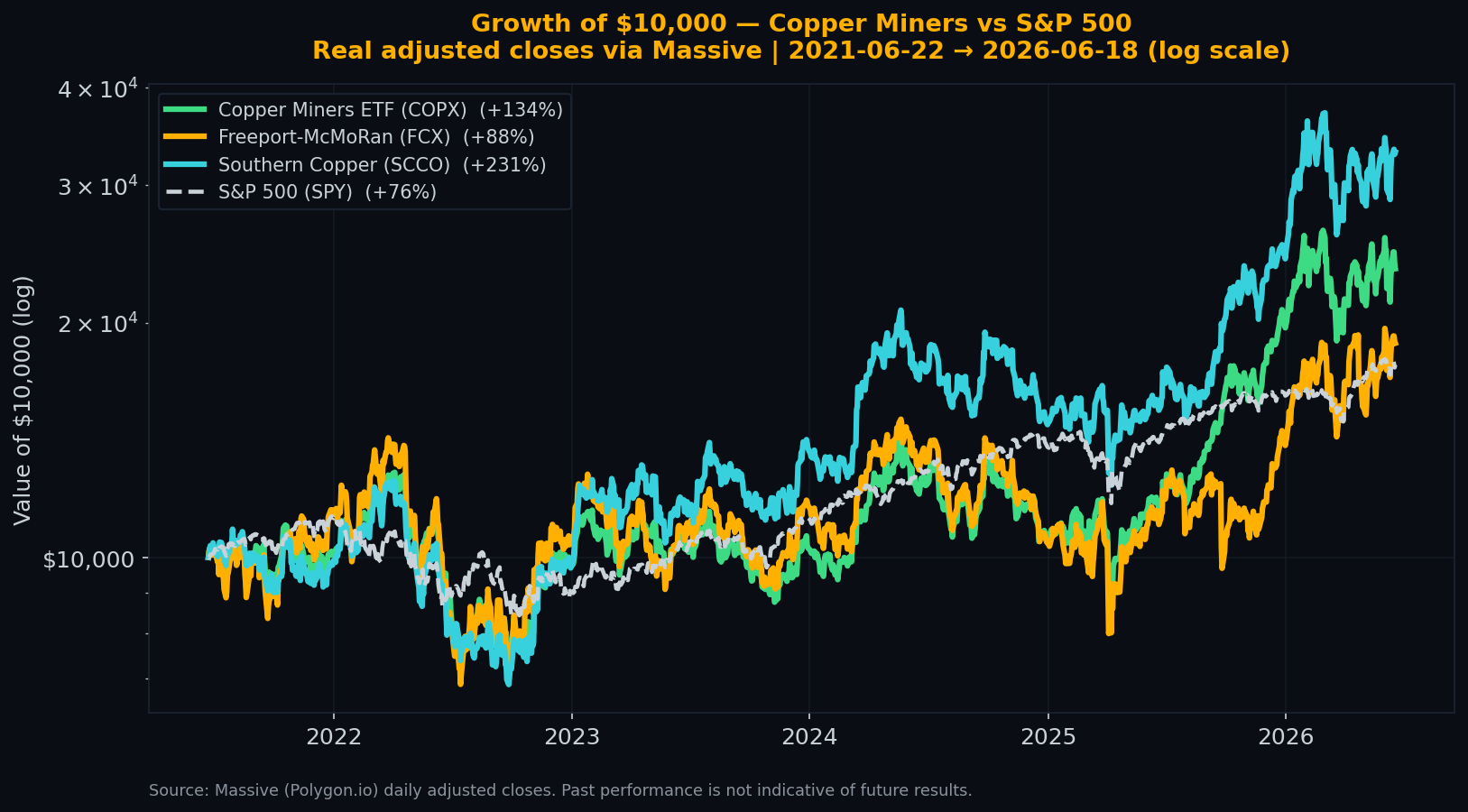

Diversified Majors and ETFs: For broad exposure, the market leans on major producers like Freeport-McMoRan (FCX) and Southern Copper (SCCO), or the Global X Copper Miners ETF (COPX). These entities hold massive, established reserves that become increasingly valuable as the deficit widens.

The Zambia / Copperbelt Players: For targeted exposure to the African scramble, operators like First Quantum Minerals (FM.TO)—which recently opened a $1.25 billion expansion at its Kansanshi mine in Zambia [4]—and Barrick Gold are deeply entrenched in the region. On the private side, US-backed exploration firms like KoBold Metals are actively hunting for the next major Copperbelt deposit [5].

The Honest Read: Volatility and Execution Risk

The standard disclaimer applies: This is not investment advice. It is an analysis of systemic constraints.

If you look at the performance chart above, the reality of mining equities is clear: they can outperform the broader market, but they do so with violent volatility. Over the roughly five-year window charted, Southern Copper (SCCO) delivered a +231% return, but investors had to stomach a −45% maximum drawdown along the way. Freeport-McMoRan (FCX) suffered a −51% drawdown. The Copper Miners ETF (COPX) fell by −43%.

Furthermore, the Zambian pivot carries immense execution risk. Zambia missed its 1-million-tonne target in 2025 [5]. The country relies on hydropower for 85% of its electricity; recent severe droughts have forced miners to secure expensive emergency diesel generation, adding roughly $0.07 per pound to their costs [4].

Finally, the deficit is a projection, not a prophecy—and high prices cure high prices. If copper runs to $6 or $7 a pound, the market will respond with demand destruction, aluminum substitution in grid wiring and power cables, and a wave of scrap recycling. This is not a flaw in the thesis; it is the mechanism by which the thesis pays out. The shortfall does not have to physically materialize in 2040 for the repricing to happen—the anticipation of it is what drives copper and copper equities higher in the years before any gap is ever realized.

But substitution and recycling have hard ceilings. Aluminum already replaces copper in many overhead lines and some power cables—but it is a poor substitute where space, weight, and efficiency matter most: it carries far less current per unit volume, runs hotter, and forces bulkier designs, which is why high-performance motors, fine windings, and dense data-center busbars stay on copper despite the price gap. Recycling already supplies roughly a third of copper, but secondary supply scales slowly and is itself a function of the decades-old copper already installed—you cannot recycle metal that was never mined. So the counter-forces blunt the deficit—they do not erase it. The core constraint remains physical: you cannot print copper, and you cannot software-update a mine into existence. Until the industry compresses a 17-year lead time into a fraction of that span, the chokepoint holds firm—and the geopolitical scramble for the Copperbelt will only intensify.

The Bear Case: What Would Break This Thesis?

Every structural thesis has a failure mode. For copper, the primary risks that could break or delay the cascade are:

- Severe Demand Destruction: A deep, synchronized global recession that halts the AI data center buildout and the broader electrification transition, pushing the projected 10 Mt deficit out by a decade.

- Breakthrough Substitution: A sudden, scalable commercialization of carbon nanotubes, graphene, or advanced aluminum alloys that can replace copper in high-voltage transmission without the thermal penalties.

- Deep-Sea Mining Legalization: If the International Seabed Authority (ISA) unexpectedly greenlights the commercial harvesting of polymetallic nodules, unlocking the estimated 21 billion tonnes of copper on the ocean floor and crashing the scarcity premium.

References

- S&P Global. “Substantial Shortfall in Copper Supply Widens as the Race for AI and Growing Defense Spending Add to Accelerating Demand.” January 8, 2026.

- International Energy Agency (IEA). Global Critical Minerals Outlook 2025 — projects a ~30% copper supply deficit by 2035 (current policies), widening to ~40% in a net-zero scenario. (Reported via Argus Media and Global Trade Review.)

- Reuters. “Global power grid expansion fuels fresh copper demand surge.” July 31, 2025.

- Mining Technology. “Kansanshi S3: Zambia’s biggest copper investment in a decade.” September 5, 2025.

- Reuters / CNBC Africa. “Zambia seeking global investors to help triple copper output by 2031.” March 10, 2026.

- European Commission, International Partnerships. “Connecting the Democratic Republic of the Congo, Zambia, and Angola to global markets through the Lobito Corridor.”

Liquidity & size of the names above

Data as of 2026-06-26 · Massive/Polygon, last ~30 trading days · figures move daily

Real figures from market data (2026-06-23 (last ~30 trading days)). Size tiers reflect median daily dollar volume — how easily a position can actually be entered or exited. This is reference data, not a recommendation.

Liquidity, in plain terms: how easily you can get in and out. Deep means you can trade freely without moving the price; Thin means even small orders can move it — mind the spread.

What this does not tell you — valuation. A real structural deficit does not mean the price hasn’t already discounted it. These figures show size and tradeability only; we deliberately do not screen for valuation, solvency, or whether a name is cheap or expensive today. Do your own valuation work.

| Ticker | Name | Type | Market cap | Median daily $ vol | Liquidity |

|---|---|---|---|---|---|

| FCX | Freeport-McMoran Inc.~80% of revenue is copper; gold (Grasberg) and molybdenum are byproducts. Largest US-listed copper pure-ish play. | Stock | $98.7B | $879.0M | Deep |

| SCCO | Southern Copper CorporationOne of the purest copper majors (Peru/Mexico), but ~88% owned by Grupo México — low free float, controlled-company governance risk. | Stock | $161.0B | $248.4M | Deep |

| COPX | Global X Copper Miners ETF (NEW)Pure copper-miner ETF, ER 0.65%, ~$8B AUM, 41 holdings; globally diversified (KGHM, Teck, BHP, First Quantum, Antofagasta) — FCX/SCCO each only ~5%. | ETF | n/a · ETF | $337.7M | Deep |

Tiers: Deep ≥ $100M/day · Liquid $20–100M · Moderate $3–20M · Thin $1–3M · < $1M = execution risk. The note under each name is a sourced exposure disclosure (how pure or diluted the play is), not a valuation view. Source: Massive/Polygon aggregates, last ~30 trading days (snapshot 2026-06-26). Figures move daily.

Found this useful? AtomProphet is independent and reader-funded — you can support the research & hosting ↓

Get the next cascade in your inbox

One short email when a new analysis drops — a single constraint traced end to end, from the physics to the chokepoint to the tickers, with the honest bear case kept in view. No marketing, no tracking, no noise.

- One email per published analysis — typically a few a month, never a daily blast

- The full cascade: driver → chokepoint → vetted, live-liquidity tickers

- The counter-case spelled out, not buried

No account, no paywall. Double opt-in, and one-click unsubscribe in every email.

Support the research & hosting

AtomProphet is independent, ad-light, and reader-funded. Contributions help cover data feeds, hosting, and the time behind the Cascade Graph — they keep this research free and open. A tip buys nothing, unlocks nothing, and is not payment for advice or for any security mentioned anywhere on this site.

Bitcoin37h98hpiHz6BW6ELvRLagk7BBo8UUtxeSh USDC · Base 0x1ac1Abe9eCAd5fAd8fF55B188E079b52cD1e6415