The Nuclear Inevitability: Why AI's Power Hunger Ends the Renewables-Only Dream

The artificial intelligence revolution is on a structural collision course with the hard limits of electrical physics.

For the past decade, the prevailing narrative in energy policy has been a linear, painless transition to intermittent renewables—wind and solar—supported by grid-scale battery storage. This model, while politically palatable, is mathematically incapable of supporting the next phase of technological and industrial development.

Under The Cascade Thesis, the exponential growth of AI compute requirements creates an inescapable bottleneck: the demand for continuous, high-density baseload power. The only technology capable of meeting this demand at scale, without accelerating climate breakdown, is nuclear energy. The market is only just beginning to wake up to the math.

The Staggering Math of AI Data Centers

Data centers are not traditional industrial loads. They operate 24/7/365 with near-100% utilization rates. They cannot be powered by energy sources that disappear when the sun sets or the wind dies.

The International Energy Agency (IEA) projects that global electricity consumption for data centers will more than double to roughly 945 terawatt-hours (TWh) by 2030 [1]. To put that in perspective, 945 TWh is about the entire annual electricity consumption of Japan—the world’s fourth-largest economy—added to the grid in barely five years.

This growth is driven almost entirely by the deployment of high-performance accelerated servers required for AI training and inference. According to the IEA, electricity consumption by these AI-specific servers is growing at 30% annually, accounting for nearly half of the net increase in global data center power demand [1]. In the United States alone, data center power consumption is expected to increase by 130% by the end of the decade.

The Illusion of “100% Renewable” Tech Giants

Major technology companies frequently claim to operate on “100% renewable energy.” This is an accounting fiction achieved through the purchase of Renewable Energy Certificates (RECs).

When a hyperscale data center demands 500 megawatts of continuous power at 2:00 AM on a windless night, it is not running on solar or wind. It is drawing power directly from the local grid’s baseload—which, in most of the world, means burning natural gas or coal. Purchasing a solar REC from a farm a thousand miles away does not alter the physical reality of the electrons entering the server racks.

As tech giants face the physical constraints of the grid, they are realizing the renewables-only model is insufficient for baseload. They are not abandoning wind and solar—they are doing both—but they now recognize that securing guaranteed, 24/7 nuclear power is no longer just a sustainability metric, it is a primary competitive moat.

The Uranium Supply Deficit and the “Lost Decade”

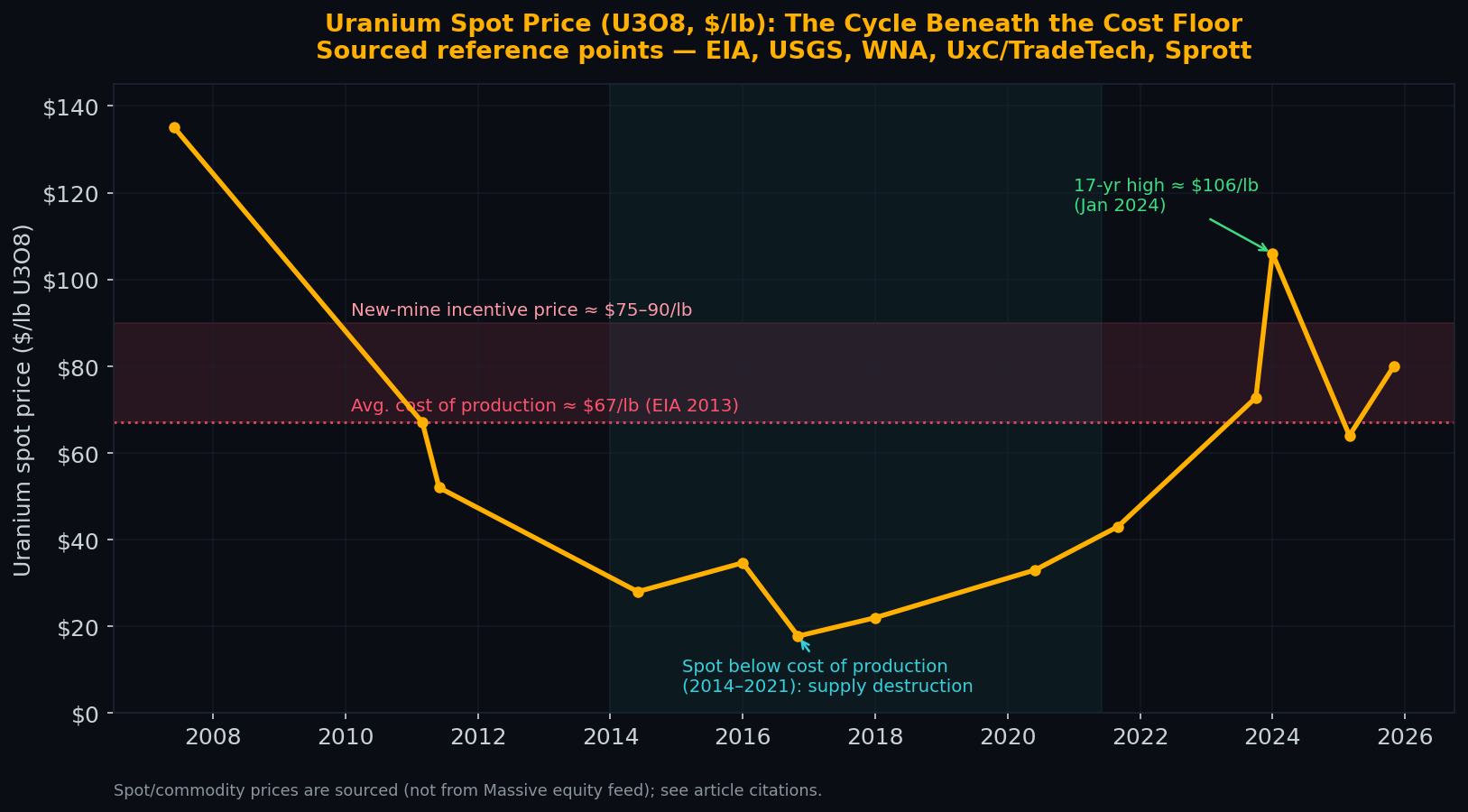

To understand why the current nuclear renaissance is so explosive for uranium equities, we must look at the “lost decade” that preceded it. Following the 2011 Fukushima disaster, the global uranium market collapsed into a severe, prolonged bear market.

By 2016, the spot price of uranium plummeted below $18 per pound [3] — far below the marginal cost of production for almost every mine on earth, which typically ranges from $50 to $70 per pound [4].

The spot price spent years below the cost of production, destroying supply capacity before the AI demand shock arrived.

Because it cost more to mine uranium than to sell it, producers did the only rational thing: they shut down mines, canceled exploration, and starved the sector of capital. This created a massive, structural supply deficit that was temporarily masked by the drawdown of secondary stockpiles.

The World Nuclear Association (WNA) projects that global uranium requirements for reactors will rise by a third to 86,000 tonnes by 2030, and to 150,000 tonnes by 2040 [2].

Crucially, this demand surge coincides with that structural supply deficit. The WNA warns that output from currently operating mines is expected to halve between 2030 and 2040 as existing deposits are exhausted [2]. Today, the shortfall between mine output and reactor demand is bridged by secondary supplies—existing stockpiles and recycled material—which currently cover roughly 11–14% of reactor requirements. But the WNA projects that cushion thinning to just 4–11% by 2050 [2]. The buffer that has masked the deficit is running out.

The Investment Reality

The intersection of AI’s insatiable power demand and the structural deficit in uranium supply creates one of the most asymmetric investment setups of the decade.

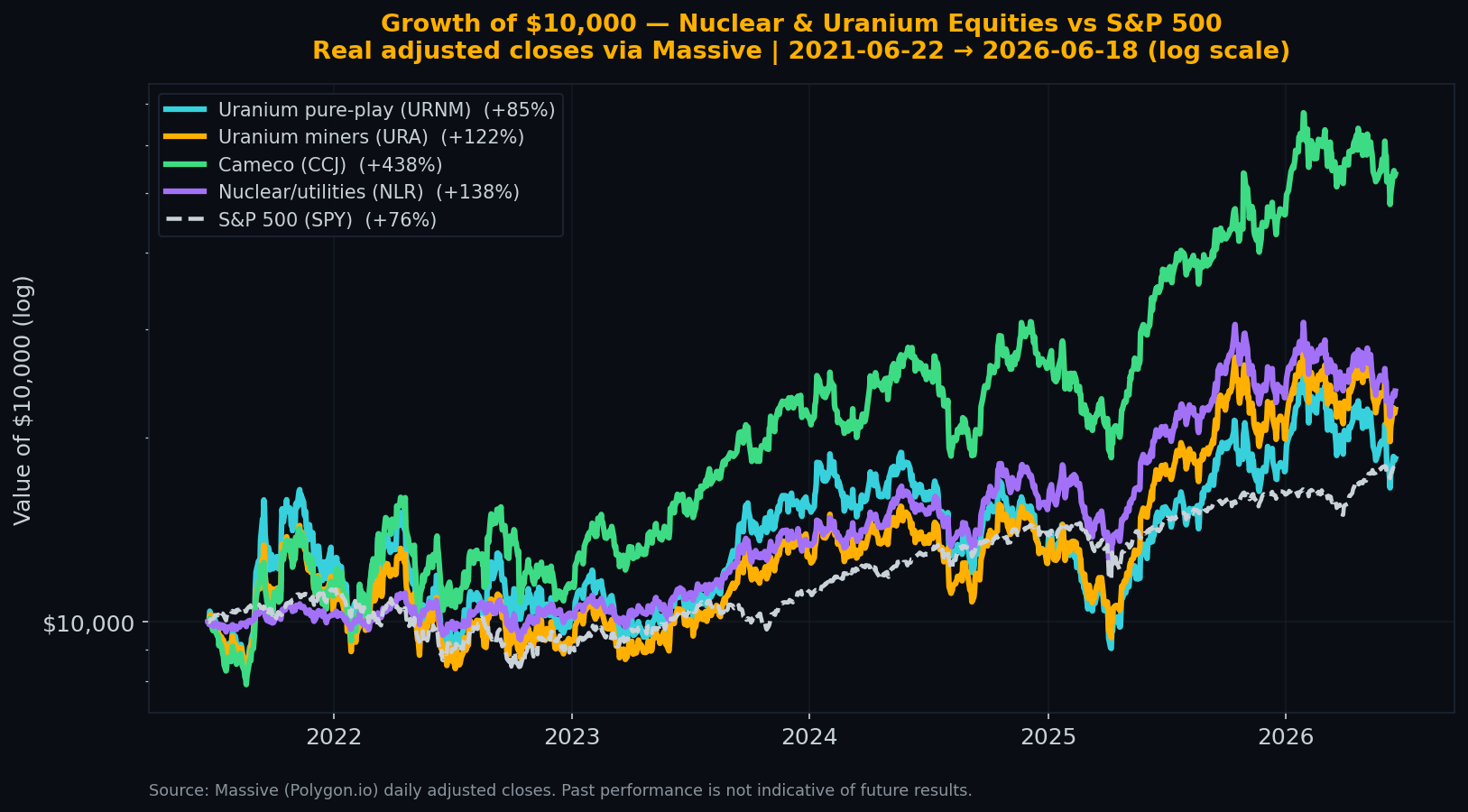

The market has begun to price this in. When the realization hit that the “lost decade” of supply destruction was colliding with the AI demand shock, capital flooded into the few surviving producers.

Over the past five years, the nuclear sector has decisively beaten the S&P 500, led by tier-one producers like Cameco (+438%). However, note the severe drawdowns (40%+) inherent to the sector.

While the 122% return of the Global X Uranium ETF (URA) and Cameco’s 438% run over our five-year study window are spectacular, this is not a trade for the faint of heart. The risk caveat is explicit: as the chart shows, every major uranium sleeve—URA, the URNM pure-play ETF, and Cameco itself—suffered a drawdown of roughly 40% to 52% during this period. Uranium equities are famously volatile, prone to violent washouts, and acutely sensitive to political shifts and supply shocks. The returns are real; so is the pain required to capture them.

But the physical realities of mine development mean the supply response will take years to materialize. It takes 10 to 15 years to permit and build a new uranium mine. You cannot solve a physical deficit with software updates or financial engineering.

Furthermore, the development of Small Modular Reactors (SMRs), specifically designed to co-locate with data centers, represents a massive future demand vector. However, SMRs are realistically a 2035+ story; they will not solve the immediate power crunch of the next five years, making the strain on the existing nuclear fleet even more acute.

The mathematics are unforgiving. You can have exploding AI-driven baseload demand, or you can insist on a grid powered exclusively by intermittent renewables. You cannot have both. Wind and solar will keep growing—but the 24/7 baseload that AI demands belongs to the atom, and the uranium to fuel it is already running short.

The Bear Case: What Would Break This Thesis?

Every structural thesis has a failure mode. For uranium and nuclear baseload, the primary risks that could break or delay the cascade are:

- Another Major Reactor Incident: A severe safety incident at any global nuclear facility would instantly freeze public sentiment, halt new builds, and likely trigger a politically-driven phaseout akin to the post-Fukushima “lost decade.”

- AI Efficiency Breakthroughs: A paradigm shift in AI hardware or model architecture (e.g., optical computing, radically more efficient algorithms) that decouples compute scaling from power scaling, collapsing the projected 945 TWh data center demand.

- Massive Over-Contracting Reversal: If utilities have double-booked or over-contracted uranium in panic, a sudden release of secondary supply or a coordinated drawdown of strategic stockpiles could temporarily crash the spot price below the marginal cost of production.

References

[1] International Energy Agency (IEA). (2025). “Energy and AI.” https://www.iea.org/reports/energy-and-ai

[2] World Nuclear Association (WNA). (2025, September 5). “Nuclear Renaissance Could Create Shortage Of Uranium Supply.” NucNet. https://www.nucnet.org/news/nuclear-renaissance-could-create-shortage-of-uranium-supply-says-wna-9-5-2025

[3] U.S. Energy Information Administration (EIA). (2017). “Uranium spot prices fell to a 12-year low in 2016.” https://www.eia.gov/todayinenergy/detail.php?id=31432

[4] World Nuclear Association (WNA). (2023). “Uranium Markets.” https://world-nuclear.org/information-library/nuclear-fuel-cycle/uranium-resources/uranium-markets

Liquidity & size of the names above

Data as of 2026-06-26 · Massive/Polygon, last ~30 trading days · figures move daily

Real figures from market data (2026-06-23 (last ~30 trading days)). Size tiers reflect median daily dollar volume — how easily a position can actually be entered or exited. This is reference data, not a recommendation.

Liquidity, in plain terms: how easily you can get in and out. Deep means you can trade freely without moving the price; Thin means even small orders can move it — mind the spread.

What this does not tell you — valuation. A real structural deficit does not mean the price hasn’t already discounted it. These figures show size and tradeability only; we deliberately do not screen for valuation, solvency, or whether a name is cheap or expensive today. Do your own valuation work.

| Ticker | Name | Type | Market cap | Median daily $ vol | Liquidity |

|---|---|---|---|---|---|

| URA | Global X Uranium ETFMost liquid uranium ETF, ER 0.69%, ~$6.6B AUM — but NOT pure uranium: ~25% industrials incl. reactor/SMR & components names, not just miners. | ETF | n/a · ETF | $191.1M | Deep |

| URNM | Sprott Uranium Miners ETFPurer uranium-miner exposure than URA (miners + physical uranium holdings), but lower liquidity and higher single-name concentration. | ETF | n/a · ETF | $37.2M | Liquid |

| CCJ | Cameco CorporationLargest Western uranium producer; also owns ~49% of Westinghouse (reactor services), so it is partly a nuclear-services play, not pure mined uranium. | Stock | $46.4B | $330.8M | Deep |

Tiers: Deep ≥ $100M/day · Liquid $20–100M · Moderate $3–20M · Thin $1–3M · < $1M = execution risk. The note under each name is a sourced exposure disclosure (how pure or diluted the play is), not a valuation view. Source: Massive/Polygon aggregates, last ~30 trading days (snapshot 2026-06-26). Figures move daily.

Found this useful? AtomProphet is independent and reader-funded — you can support the research & hosting ↓

Get the next cascade in your inbox

One short email when a new analysis drops — a single constraint traced end to end, from the physics to the chokepoint to the tickers, with the honest bear case kept in view. No marketing, no tracking, no noise.

- One email per published analysis — typically a few a month, never a daily blast

- The full cascade: driver → chokepoint → vetted, live-liquidity tickers

- The counter-case spelled out, not buried

No account, no paywall. Double opt-in, and one-click unsubscribe in every email.

Support the research & hosting

AtomProphet is independent, ad-light, and reader-funded. Contributions help cover data feeds, hosting, and the time behind the Cascade Graph — they keep this research free and open. A tip buys nothing, unlocks nothing, and is not payment for advice or for any security mentioned anywhere on this site.

Bitcoin37h98hpiHz6BW6ELvRLagk7BBo8UUtxeSh USDC · Base 0x1ac1Abe9eCAd5fAd8fF55B188E079b52cD1e6415