The Northern Pivot: Opportunities in the Arctic as the World Warms

The map of global commerce is being structurally redrawn by thermodynamics.

For centuries, the Arctic has been a frozen, impassable barrier. Today, it is the site of the most rapid environmental transformation on Earth, warming nearly four times faster than the global average [1]. This phenomenon, known as Arctic Amplification, is dismantling the ice cap and, with it, the traditional geographic constraints on shipping, resource extraction, and military posture.

Under the framework of The Cascade Thesis, climate change is not merely an ecological event; it is a structural economic catalyst. The thawing of the Arctic presents a profound, asymmetric investment frontier—but only if you understand the difference between the physical reality and the financial mirage. It requires distinguishing between long-term infrastructure shifts and immediate equity returns.

The Mathematics of the Melt

The data regarding Arctic sea ice decline is unequivocal. According to the National Oceanic and Atmospheric Administration (NOAA) and the National Snow and Ice Data Center (NSIDC), the September summer minimum sea ice extent has been declining at a rate of roughly 12.7% per decade since the satellite record began in 1979 [2].

More critically, the Arctic is losing its old, thick ice. NOAA’s 2025 Arctic Report Card finds that today’s ice cover holds about 47% less multiyear ice—the resilient ice that survives the summer melt—than it did in the 1980s, leaving an ice pack that is far younger, thinner, and far more susceptible to rapid seasonal melting [2].

This is not a temporary anomaly; it is a permanent phase shift. The economic implications of an accessible Arctic ocean are staggering.

The Northern Sea Route (NSR)

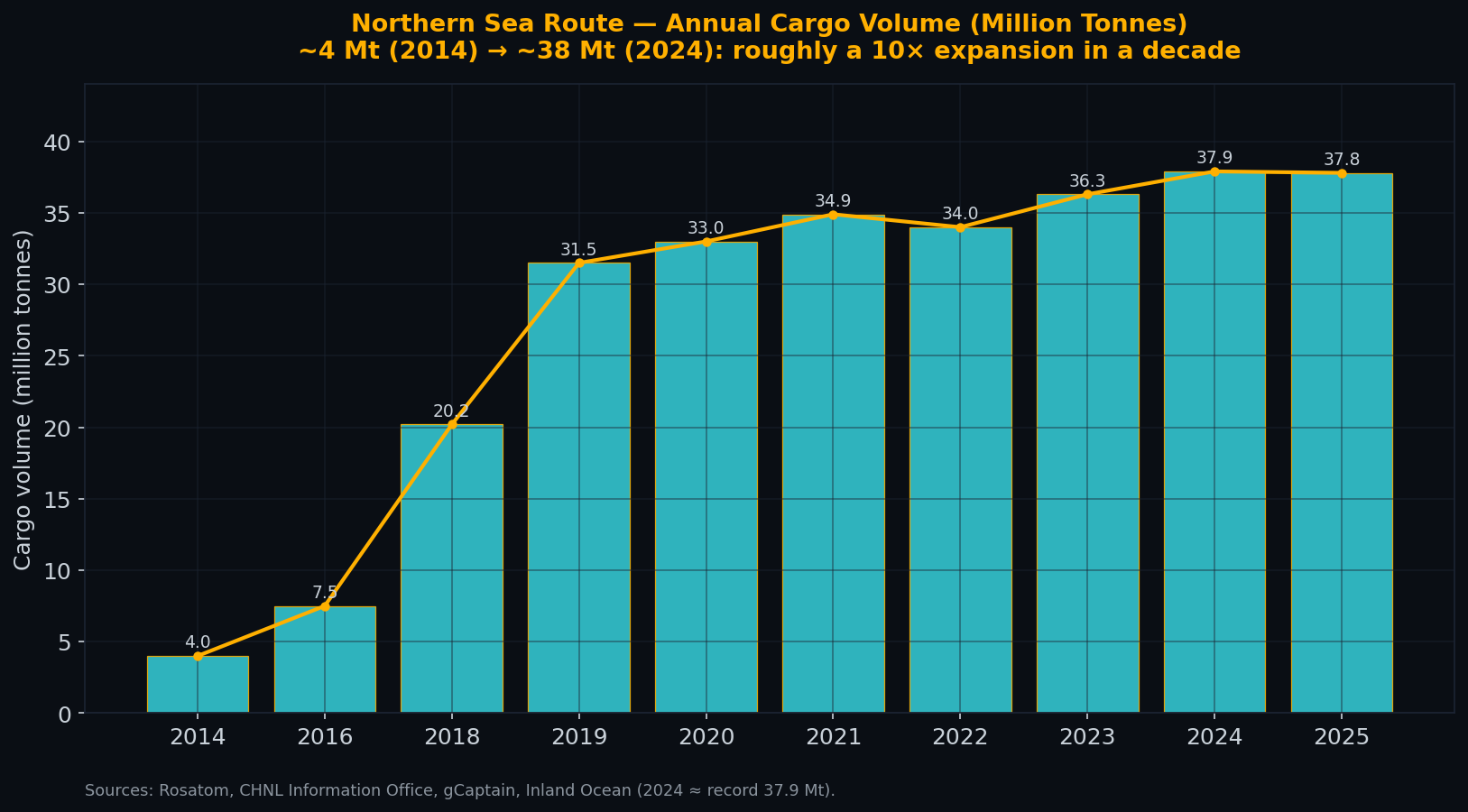

The most immediate economic impact of a warming Arctic is the viability of the Northern Sea Route (NSR). Running along the Russian Arctic coast, the NSR offers a shortcut between Asian manufacturing hubs and European markets, reducing transit distances by up to 50% compared to the traditional Suez Canal route [3].

The allure of the NSR is undeniable: shorter transit times dictate lower fuel costs and faster delivery. The physical volume of cargo moving through this once-frozen corridor tells the story better than any theoretical forecast.

Cargo volumes on the NSR expanded roughly 10x over a decade, from ~4 million tonnes in 2014 to a record ~38 million tonnes in 2024—before slipping back in 2025 and falling well short of Russia’s 80 Mt target. [4]

However, the Cascade Thesis demands rigorous realism—and the most recent data demands it loudly. After peaking near 38 million tonnes in 2024, NSR cargo volumes have now fallen for two consecutive years, slipping to roughly 37 million tonnes in 2025 and landing at less than half of Russia’s stated 80-million-tonne target for 2030 [4]. The NSR is heavily controlled by Russia, and in an era defined by geopolitical decoupling and the “friendly-shoring” of supply chains, relying on a Russian-dominated, sanction-exposed shipping lane introduces severe geopolitical risk. The physical corridor is opening; the political one is closing.

Investing in the Friendly North

The intelligent play is not to gamble on Russian shipping, but to recognize that the entire northern latitude is becoming structurally more economically viable. The focus must be strictly on friendly jurisdictions: Canada, the Nordic countries, and the United States (Alaska).

- Infrastructure and Icebreakers: As the Arctic opens, the demand for specialized maritime infrastructure—specifically icebreakers and ice-hardened commercial vessels—will surge. The US currently lags severely behind Russia in icebreaker capacity, a gap that must be closed for national security reasons. Companies involved in the design and construction of these vessels stand to benefit.

- Resource Accessibility: The receding ice and thawing permafrost are making previously inaccessible mineral deposits viable for extraction. This includes critical minerals necessary for the energy transition. Again, the focus must remain strictly on mining operations within Canadian and Nordic territories, avoiding the jurisdictional risks of Russian extraction.

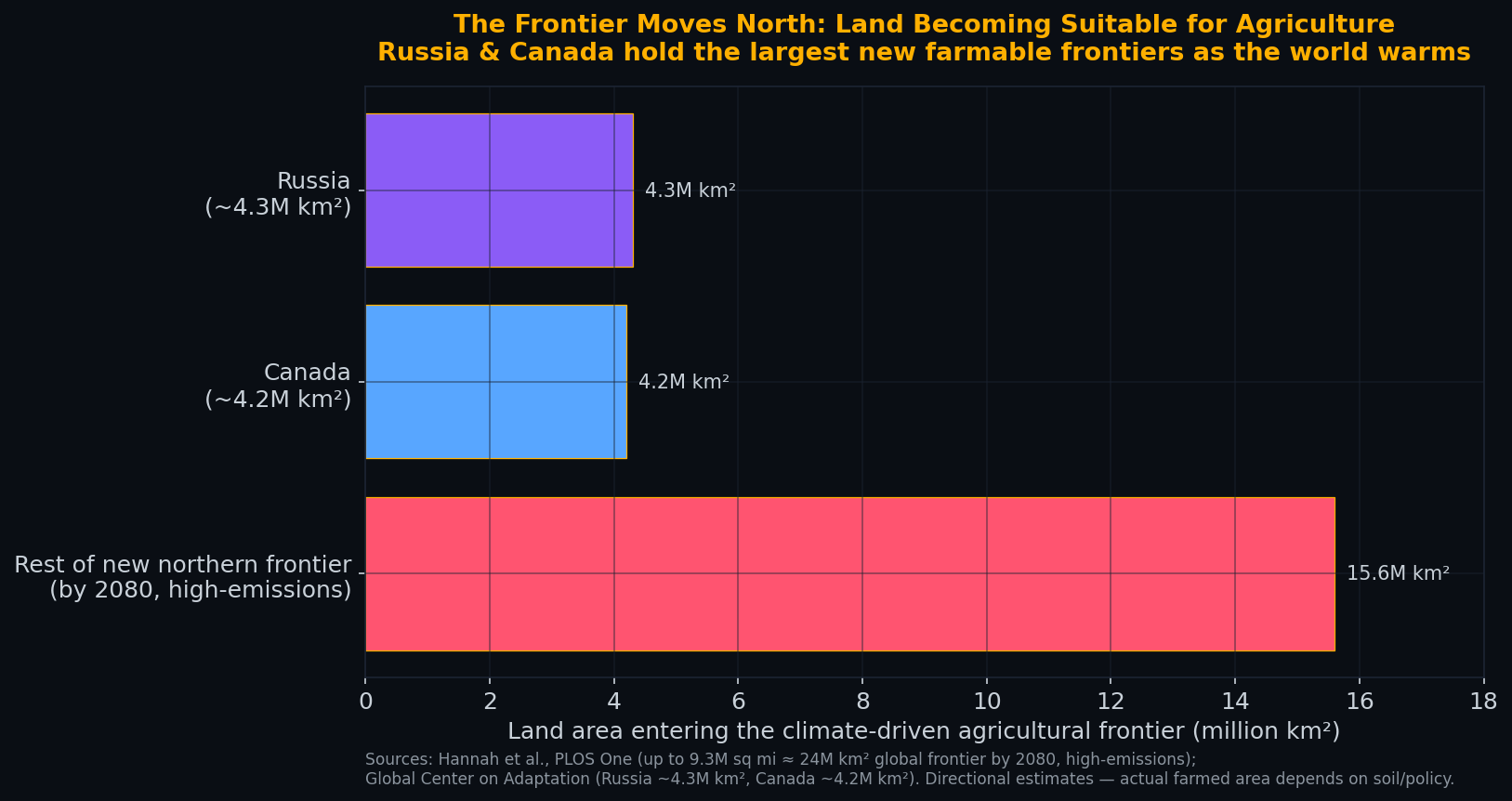

- The New Agricultural Frontier: Broad exposure to the economies of northern-latitude nations provides a macro-hedge against the impacts of warming closer to the equator. As arable land shifts northward and water stress impacts the global south, the economic gravity of nations like Canada will naturally increase.

Where the Investable Exposure Actually Is

This is where intellectual honesty matters more than a tidy ticker list. The purest expressions of the Arctic shipping thesis are, for an ordinary investor, largely uninvestable — and we would rather say so than point you at a fragile proxy:

- Arctic/maritime shipping ETFs are too thin to use. The most-cited “shipping” funds (for example the SonicShares Global Shipping ETF, BOAT, and the U.S. Global Sea to Sky Cargo ETF, SEA) trade well under $1M of median daily value — below any serious tradeability floor. A position is easy to enter and painful to exit.

- The cleanest single name, Maersk, has no good U.S. line. A.P. Møller-Maersk is properly liquid only on its home Copenhagen listing (MAERSK-B.CO); its U.S. ADR (AMKBY) trades only ~$1M/day and the ordinary OTC share (AMKBF) is effectively untradeable here.

- The purest Arctic-shipping exposure of all — the Russian Northern Sea Route operators (Sovcomflot, Novatek’s Arctic LNG) — is sanctioned and off-limits.

So the honest terminal node for this thesis is not shipping at all; it is the northern-cropland / agribusiness leg, where real, liquid, accessible names exist:

- DE — Deere & Co. The dominant farm-equipment maker; direct leverage to expanding northern arable acreage. Deeply liquid (~$748M median daily value).

- AGCO — AGCO Corp. A pure-play global farm-equipment maker (Fendt, Massey Ferguson); a cleaner, smaller agriculture bet than Deere. Liquid (~$73M/day).

- MOO — VanEck Agribusiness ETF. The diversified, low-effort way to own the agribusiness chain (equipment, fertilizer, seeds, processors) rather than a single stock.

Each of these is screened, real-data-verified, and labelled with its honest size and liquidity in the reference table below. Note the equity caveat that follows: even these names have not outperformed the S&P over the last five years — this remains a long-horizon, physical-asset thesis, not a crowded trade. We deliberately name no Arctic-shipping ticker, because no clean, liquid, accessible public pure-play exists today; if one emerges, we will add it.

A 2020 study in PLOS One modeled that under high-emissions scenarios, up to 9.3 million square miles (roughly 24 million km²) of land globally could enter the climate-driven agricultural frontier by 2080 [6]. A separate analysis by the Global Center on Adaptation found that Russia and Canada hold the vast majority of this newly suitable land.

The physical geography of agriculture is shifting north. Canada and Russia are the undisputed heavyweights of the new farmable frontier. [6] [7]

The Edge: Why Naive Exposure Fails

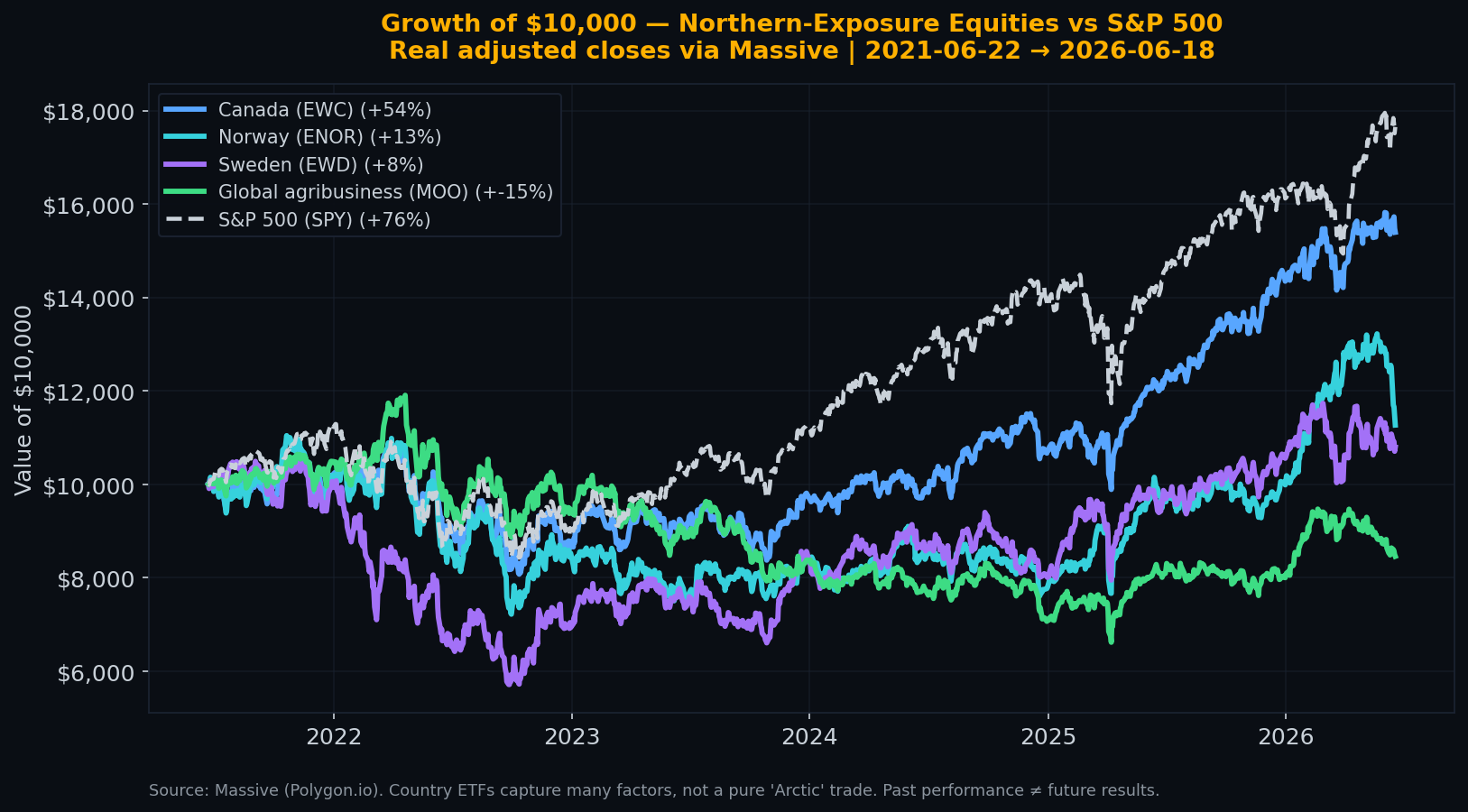

However, the Cascade Thesis demands strict financial realism alongside scientific observation. Has this physical shift translated into equity returns yet?

The honest answer: not yet. Broad northern-country ETFs and agribusiness have significantly underperformed the S&P 500 over the last five years.

This underperformance is precisely why the Arctic thesis is compelling. It is a long-horizon, physical-asset and infrastructure story — not something cleanly captured by buying a broad country-index ETF today. A broad Canada fund is heavily weighted toward banks and legacy energy, not Arctic farmland or next-generation icebreakers.

The physical trends are real and measurable, but the naive equity expression hasn’t paid off yet. It remains an under-priced, early thesis rather than a crowded trade.

The Sober Reality

It is crucial to avoid blind optimism. Arctic operations remain incredibly hostile. The environment is harsh, insurance premiums for Arctic shipping are exorbitant, and the ecological risks of an industrial accident in these pristine waters are immense.

Furthermore, a 2025 study published in Nature Communications projects that increased use of Arctic sea routes could actually raise global shipping emissions by 8.2% by 2100, with Arctic-specific emissions climbing from 0.22% to 2.72% of the global total [5].

The Arctic is opening, but it will not be a frictionless bonanza. It will be a fiercely contested, expensive, and strategically vital frontier. The structural opportunities lie in the specific infrastructure required to navigate it, the hard assets being unlocked, and the friendly jurisdictions that control it. The map is changing — and the economic weight is shifting to the right side of the ice.

The Bear Case: What Would Break This Thesis?

Every structural thesis has a failure mode. For the Arctic opening and the northern-cropland pivot, the primary risks that could break or delay the cascade are:

- Soil-Quality Reality Check: While temperatures move north, high-quality topsoil does not. If the newly thawed Canadian/Nordic land proves too acidic or rocky for high-yield mechanized farming, the agribusiness equipment boom (DE/AGCO) will not materialize as projected.

- Geopolitical Freeze: A severe escalation in Arctic militarization between NATO and Russia that turns the high north into an active exclusion zone, freezing commercial development and infrastructure investment.

- The AMOC Collapse: If Arctic meltwater shuts down the Atlantic Meridional Overturning Circulation (the Gulf Stream), northern Europe and parts of North America could actually experience severe cooling, reversing the warming trend that underpins the agricultural shift.

References

[1] Rantanen, M., et al. (2022). “The Arctic has warmed nearly four times faster than the globe since 1979.” Communications Earth & Environment, 3(168). https://doi.org/10.1038/s43247-022-00498-3

[2] National Oceanic and Atmospheric Administration (NOAA). (2025). “Arctic Report Card 2025.” https://www.arctic.noaa.gov/Report-Card/

[3] The Arctic Institute. (n.d.). “The Northern Sea Route.” https://www.thearcticinstitute.org/

[4] CHNL / Inland Ocean. (2025). “NSR Shipping Traffic Data.”

[5] Li, X., et al. (2025). “Arctic Sea Route access reshapes global shipping carbon emissions.” Nature Communications, 16. https://doi.org/10.1038/s41467-025-64437-4

[6] Hannah, L., et al. (2020). “Shifting cultivation geographies in the Central and Northern Americas.” PLOS One.

[7] Global Center on Adaptation. (2020). “Ice is melting on fertile Canadian land.”

Liquidity & size of the names above

Data as of 2026-06-26 · Massive/Polygon, last ~30 trading days · figures move daily

Real figures from market data (2026-06-23 (last ~30 trading days)). Size tiers reflect median daily dollar volume — how easily a position can actually be entered or exited. This is reference data, not a recommendation.

Liquidity, in plain terms: how easily you can get in and out. Deep means you can trade freely without moving the price; Thin means even small orders can move it — mind the spread.

What this does not tell you — valuation. A real structural deficit does not mean the price hasn’t already discounted it. These figures show size and tradeability only; we deliberately do not screen for valuation, solvency, or whether a name is cheap or expensive today. Do your own valuation work.

| Ticker | Name | Type | Market cap | Median daily $ vol | Liquidity |

|---|---|---|---|---|---|

| MOO | VanEck Agribusiness ETFDiversified agribusiness (equipment, fertilizer, seeds, processors); the low-effort way to own the northern-cropland leg. | ETF | n/a · ETF | $18.0M | Moderate |

| DE | Deere & CompanyDominant farm-equipment maker; direct leverage to expanding northern arable acreage. Cyclical to ag capex, not a pure 'Arctic' name. | Stock | $159.1B | $748.1M | Deep |

| AGCO | AGCO CorporationPure-play global farm-equipment maker (Fendt, Massey Ferguson); smaller, cleaner ag-equipment bet than Deere; more cyclical. | Stock | $8.2B | $72.7M | Liquid |

Tiers: Deep ≥ $100M/day · Liquid $20–100M · Moderate $3–20M · Thin $1–3M · < $1M = execution risk. The note under each name is a sourced exposure disclosure (how pure or diluted the play is), not a valuation view. Source: Massive/Polygon aggregates, last ~30 trading days (snapshot 2026-06-26). Figures move daily.

Found this useful? AtomProphet is independent and reader-funded — you can support the research & hosting ↓

Get the next cascade in your inbox

One short email when a new analysis drops — a single constraint traced end to end, from the physics to the chokepoint to the tickers, with the honest bear case kept in view. No marketing, no tracking, no noise.

- One email per published analysis — typically a few a month, never a daily blast

- The full cascade: driver → chokepoint → vetted, live-liquidity tickers

- The counter-case spelled out, not buried

No account, no paywall. Double opt-in, and one-click unsubscribe in every email.

Support the research & hosting

AtomProphet is independent, ad-light, and reader-funded. Contributions help cover data feeds, hosting, and the time behind the Cascade Graph — they keep this research free and open. A tip buys nothing, unlocks nothing, and is not payment for advice or for any security mentioned anywhere on this site.

Bitcoin37h98hpiHz6BW6ELvRLagk7BBo8UUtxeSh USDC · Base 0x1ac1Abe9eCAd5fAd8fF55B188E079b52cD1e6415