The Uninsurable Future: Profiting from the Climate Risk-Transfer Boom

The physical economy breaks first where the risk models fail.

In California, Florida, Louisiana, and increasingly across Europe, the primary property insurance model is fracturing. Driven by the rising frequency and severity of insured catastrophes—wildfires, floods, and severe convective storms—major carriers are non-renewing policies, spiking premiums, and abandoning peak-risk zones entirely. In California alone, premiums have jumped 84% since 2020, forcing homeowners into ballooning state-backed insurers of last resort.

But the capital doesn’t disappear; it reorganizes. The risk that primary insurers refuse to hold on their balance sheets is being aggressively transferred upward into the reinsurance towers, and ultimately, into the capital markets.

Welcome to the golden age of the catastrophe bond.

The Mechanism: The $41 Trillion Protection Gap

The causal chain is mechanical and already visible in the Cascade Graph: Warming & Hydrological Change and Extreme Heat drive catastrophe losses, which strain Climate Insurance, forcing a hard reinsurance market that drives demand for the Catastrophe Bond & ILS Market.

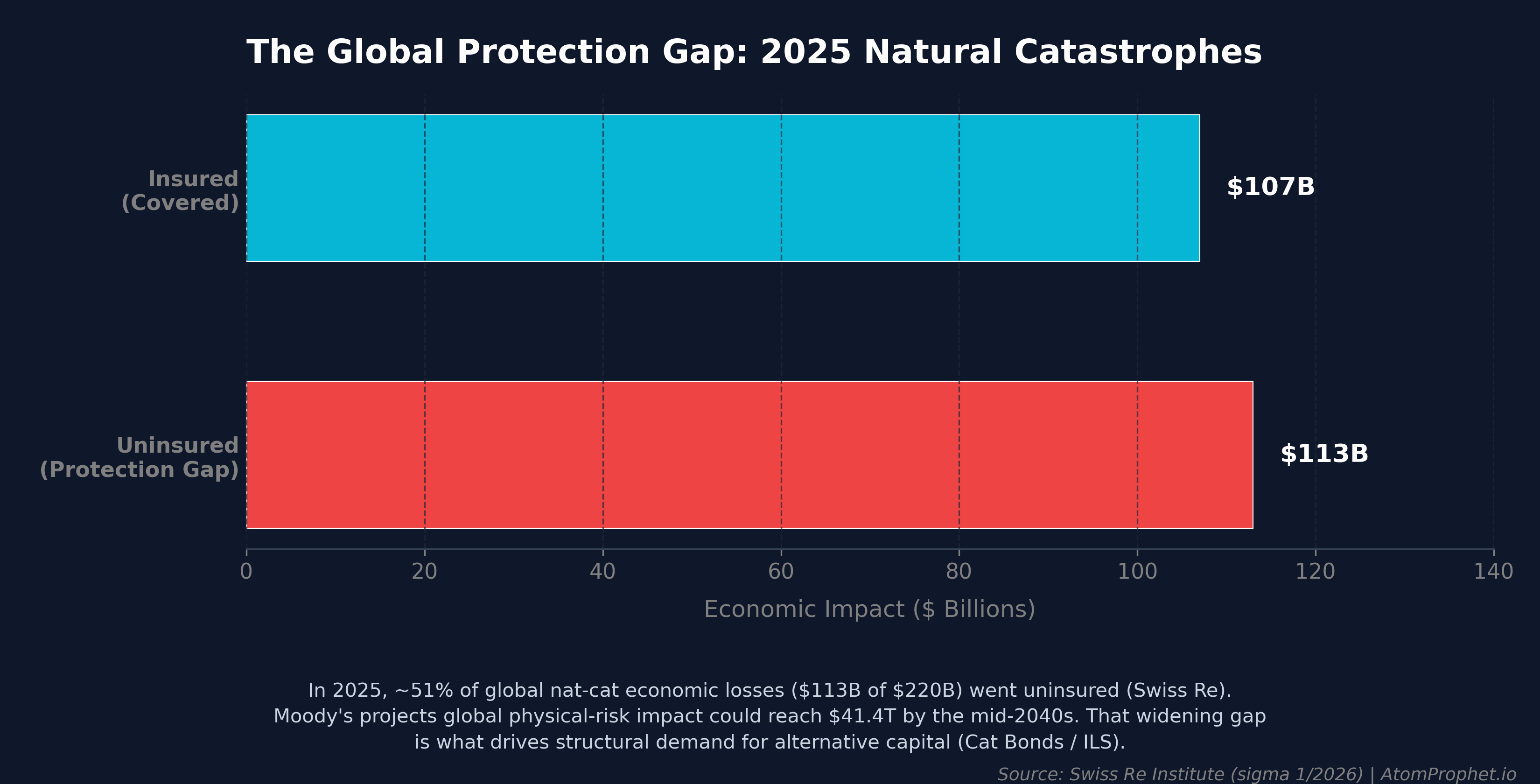

The scale of this shift was laid bare this quarter. According to Moody’s, the global economic impact of physical climate risk could reach an astonishing $41.4 trillion by the mid-2040s [1]. Yet the insurance industry is failing to keep pace. The Swiss Re Institute counts $220 billion in global natural-catastrophe economic losses for 2025, of which only $107 billion—roughly 49%—was insured; the remaining $113 billion fell on governments, businesses, and households [2]. Aon’s broader tally is even larger, at $260 billion in economic losses against $127 billion insured [3]. Either way, more than half the damage was uninsured, and the gap is structurally widest exactly where the hazard is growing fastest: during the 2025 European heatwave—a stretch of “temperature whiplash” in which Western Europe swung more than 12°C in ten days—an estimated 95% of losses were entirely uninsured [1].

Insurance-linked securities (ILS) and catastrophe (cat) bonds exist to close this gap. They allow insurers and reinsurers to offload peak tail-risk directly to institutional investors. If a specified disaster (e.g., a named hurricane hitting Miami with a certain wind speed) occurs, the bond is “triggered” and the investor loses their principal, which is used to pay the insurance claims. If the disaster does not occur, the investor earns a hefty, uncorrelated yield.

Because primary insurers are terrified of climate-driven tail risk, they are paying a premium to shed it. The result is a structural boom in issuance, echoing Aon CEO Greg Case’s recent call for the industry to bring “record levels of capital” and “increasingly diverse alternative risk transfer solutions” to the market [3]:

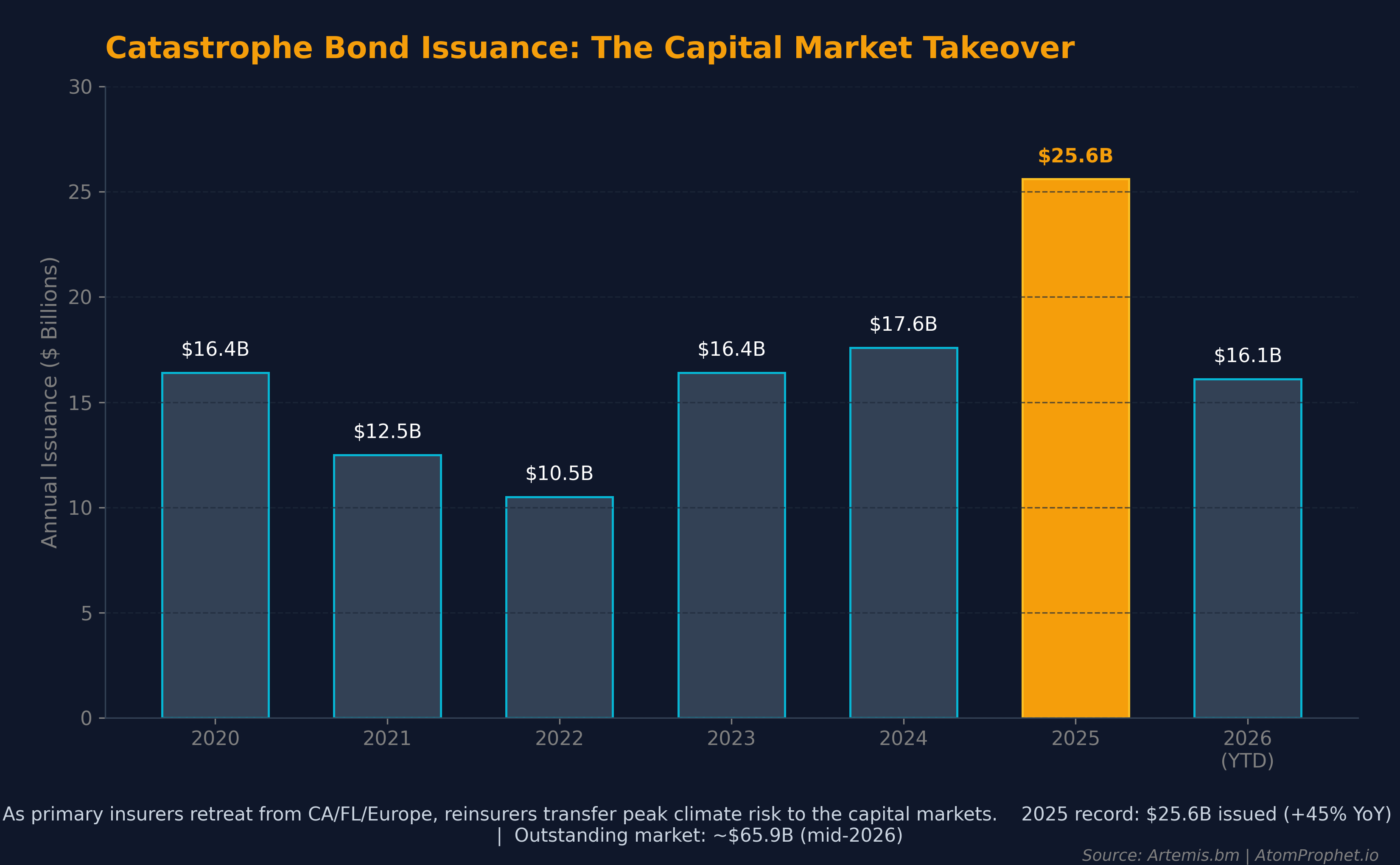

- 2025 was a record year: Total cat bond issuance hit $25.6 billion, a 45% year-over-year jump across 122 deals [4].

- The market is scaling: By mid-2026, the outstanding cat bond market reached approximately $65.9 billion [4].

- Expanding perils: Historically dominated by Florida hurricanes and California earthquakes, the market is rapidly expanding to cover secondary perils like wildfire, severe convective storms, and even cyber risk. This matters because secondary perils—not hurricanes—now drive the losses: Swiss Re reports they accounted for a record 92% of insured catastrophe losses in 2025 [2].

How These Instruments Actually Work (and Where the Risk Really Sits)

Catastrophe bonds have posted double-digit returns for three consecutive years. But to understand the risk, you must understand the mechanics. A catastrophe bond is not a monolith; its yield is exact compensation for a specific modeled expected-loss layer (the “attachment point”).

These instruments use two primary trigger mechanisms [5]:

- Indemnity triggers (roughly 75% of the market): Payouts are based on the actual, verified losses suffered by the sponsoring insurer. This eliminates basis risk for the sponsor but takes longer to settle.

- Parametric and Industry-Loss triggers: Payouts are triggered instantly if a specific physical parameter is met (e.g., a hurricane making landfall at a defined wind speed, or a regional earthquake of a specific magnitude), regardless of the insurer’s actual losses. This is faster and more transparent, but introduces basis risk—the risk that the payout does not match the actual economic damage.

The Secondary Peril Problem The models that price these bonds are highly sophisticated at predicting primary perils like a Miami hurricane or a Tokyo earthquake. But they are notoriously bad at pricing “secondary perils”—severe convective storms, localized flash floods, and wildfires. This is the structural blind spot of the asset class: secondary perils are exactly what is driving the recent surge in damage, accounting for a record 92% of insured catastrophe losses in 2025 [2].

The Honest Read: It Is Not a Free Lunch

We must be brutally honest about the mechanism: these instruments earned their recent high yields BECAUSE the peak-peril losses stayed manageable.

This is sold catastrophe insurance. A single clustered mega-catastrophe year—a Category 5 hitting Miami, followed by a historic California fire season—can and will deliver large, sudden principal losses to this asset class. The high yield is not a free lunch; it is exact compensation for bearing the tail risk that primary insurers are fleeing.

The Investable Terminals

You do not have to buy a catastrophe bond to profit from the volume of risk transfer. The cascade accrues value to several distinct layers of the market—but the honest data forces a crucial reframing. This is a forward-constraint thesis, not a victory lap. Apart from one name, these terminals have lagged the S&P 500 over the past five years, which means the mechanism’s acceleration is largely still ahead of the price, not behind it.

How directly does each profit from this? Be precise, because “climate-adjacent” is not the same as “profits from the dislocation.” The cleanest, most direct expressions are the ones that hold or manage the transferred risk: the cat-bond/ILS asset class itself (ILS), which earns the exact premium insurers pay to shed tail-risk, and RenaissanceRe (RNR), whose hard-market underwriting margins and fee-earning ILS platform both expand as the protection gap widens. The brokers (AON, MMC) are a step removed: they profit from the volume and repricing of risk transfer, clipping a fee on the flow—a robust but indirect bet that actually does best when the market is functioning and repricing, not collapsing. And a pure reinsurer (EG) is the most two-sided of all: it earns hard-market pricing but carries the catastrophe risk nakedly on its balance sheet, so a bad loss year can erase years of gains. In short: ILS and RNR are the truest expressions; the brokers are lower-beta adjacency; EG is a direct-but-risky balance-sheet bet.

| Terminal | Role | Total Return | Max Drawdown |

|---|---|---|---|

| RNR – RenaissanceRe | Reinsurer + ILS platform | +105.8% | -28.1% |

| AON – Aon plc | Broker | +31.1% | -25.5% |

| MMC – Marsh McLennan | Broker | +31.5%† | -27.7% |

| EG – Everest Group | Reinsurer | -1.2% | -26.5% |

| ILS – Brookmont Cat-Bond ETF | Direct cat-bond exposure | -2.2%‡ | -3.7% |

| SPY – S&P 500 | Benchmark | +71.8% | -25.4% |

Source: Massive (Polygon-compatible) adjusted daily closes. RNR/AON/SPY measured from 2021-06-28; EG from its 2023-07-10 feed inception; ILS from its 2025-04-01 launch. †MMC return is measured to its last available feed date (2026-01-13). ‡ILS is a young fund with ~15 months of history. Past performance is not indicative of future results.

1. The Purest Expression — The Risk-Holder (Reinsurer + ILS): RNR RenaissanceRe (RNR) is the truest equity expression of this thesis, and the only terminal here to beat the S&P (+106% vs +72%). It wins on both sides of the dislocation: hard-market reinsurance pricing—driven directly by the loss environment and primary-insurer retreat—lifts its underwriting margins, while its large third-party ILS capital platform earns capital-light fee income for managing other people’s catastrophe capital, a pool that grows as the protection gap grows. It is still genuinely two-sided—a major catastrophe year hits its own book value—but the fee-based platform is what has been rewarded.

2. The Retail Proxy (The ETF): ILS For retail investors, the asset class was historically inaccessible; institutional capital accesses this market via private 144A funds or direct reinsurance equity. That changed in April 2025 with the launch of the Brookmont Catastrophic Bond ETF (NYSE: ILS), the first US-listed, daily-tradable cat-bond ETF. Conceptually this is the most direct way to be the capital that profits from risk transfer. But be precise about what it is and is not. It is a young, relatively small retail proxy, not the source of the headline “double-digit cat-bond returns,” which describe the broad institutional indices. In its first ~15 months of trading, the ETF is modestly negative (-2.2%) with a small -3.7% drawdown. More importantly, because it is a daily-tradable ETF holding relatively illiquid underlying bonds, it carries severe liquidity and forced-selling risk. In a true mega-catastrophe event, if retail investors panic and sell the ETF simultaneously, the fund could be forced to liquidate underlying bonds into a frozen market, driving the NAV down far below the actual modeled losses.

3. The Lower-Beta Adjacency (Brokers): AON & MMC Aon (AON) and Marsh McLennan (MMC, via Guy Carpenter) are the dominant global intermediaries structuring these risk transfers. They operate on a fee-and-brokerage model—they do not hold catastrophe risk on their balance sheets, they take a cut of the surging volume of premiums and ILS issuance. This is the lower-beta, defensive adjacency: a robust bet on volume and repricing, but one step removed from the dislocation itself, and one that actually does best when the market is functioning and repricing rather than collapsing. Note the data, too: both are high-quality compounders that have trailed the index over this window (+31% vs SPY +72%), with comparable drawdowns. The bull case is volume growth and margin, not a re-rating that has already happened.

4. The Two-Sided Balance-Sheet Bet (Pure Reinsurer): EG Everest Group (EG) is an active reinsurer that benefits from hard-market pricing—but with less fee-based ILS buffer than RNR, it carries catastrophe risk more nakedly on its balance sheet. The result is the most two-sided profile here: it can profit handsomely in quiet years and get hammered in bad ones. EG is roughly flat since 2023 (-1.2%) with a ~27% drawdown despite a strong reinsurance pricing environment—a clean, sobering illustration that “the cascade is real” does not automatically mean “this stock goes up.”

The climate cascade guarantees that disaster losses will continue to rise. The insurance industry’s response guarantees that risk will be increasingly securitized. The capital markets are becoming the insurer of last resort—and the fact that most of these terminals have not yet outrun the index is precisely why the mechanism, not the past chart, is the reason to pay attention.

Valuation, Catalysts, and the Efficient Market

If the $41 trillion protection gap is public knowledge, why isn’t it already priced into these equities? And why would you buy names that have largely lagged the S&P 500?

The answer lies in the reinsurance renewal cycle and how the market values different types of risk. The market is highly efficient at pricing current earnings, but it struggles to price structural, non-linear physical phase shifts.

The Valuation Divide The performance gap between RNR and EG perfectly illustrates this. RenaissanceRe (RNR) trades near its 52-week high, at roughly a 7–9x forward P/E and above its book value. Why? Because the market is rewarding its capital-light, fee-earning ILS platform—it is clipping fees on the growing volume of third-party capital without taking all the balance-sheet risk.

Everest Group (EG), conversely, trades at a discount: roughly 0.9x book value and ~6x forward earnings. It is “cheap for a reason”—it carries the catastrophe risk nakedly on its own balance sheet. The market is discounting EG because a single clustered mega-catastrophe year could wipe out its underwriting profit. The brokers (AON, MMC) trade at premium multiples (~18x to 20x forward P/E) because they are high-quality, capital-light compounders that take a fee on volume, completely insulated from balance-sheet tail risk.

The Catalysts: The Renewal Calendar This is not a buy-and-hold-forever trade; it is deeply cyclical. The catalysts are the major reinsurance renewal dates: January 1 (global/European focus), April 1 (Japan/US), and June 1 / July 1 (Florida and US wind season).

Elevated Risk: Softening Rates Right now, the cycle is turning. After three years of a brutally hard market (sky-high premiums), the influx of alternative capital (record cat bond issuance) has actually begun to soften rates. The January 1, 2026 renewals saw risk-adjusted rate declines of roughly 14.7%, and the mid-year Florida renewals saw decreases of up to 25% on property-catastrophe lines.

This is the double-edged sword of the thesis, and a central risk factor: the mechanism is working so well that the performance-chasing capital flooding the market is compressing the yields. The next hard-market catalyst will not be a slow realization of climate change; it will be a sudden, violent repricing following the next major clustered catastrophe event that flushes this “tourist” capital out of the ILS market.

Bear Case: What Would Break This Thesis?

The structural demand for alternative capital assumes the primary insurance market continues to retreat and pass risk upward. The thesis breaks if:

- Sovereign Backstop and Political Risk: If a mega-catastrophe wipes out the primary insurers, the state will inevitably step in as the ultimate backstop. We are already seeing this ballooning risk: the California FAIR Plan’s total exposure surged 230% year-over-year to $724 billion by late 2025 [6]. If state last-resort pools collapse, governments may be forced to socialize losses broadly, rewrite the rules, and crowd out private capital entirely.

- Capital Flight: A clustered “mega-cat” year (e.g., a Category 5 hitting Miami followed immediately by historic California wildfires) triggers widespread principal losses in the ILS market, causing alternative capital to flee rather than reload.

- Model Breakthroughs: Breakthrough predictive modeling allows primary insurers to price and hold secondary-peril risk profitably again, reducing the need for reinsurance and cat bonds.

References

- Moody’s, Slow-onset climate perils are outpacing the insurance market (via Insurance Business, Jun 22, 2026) — $41.4T physical-risk impact by mid-2040s; ~95% of 2025 European heatwave losses uninsured.

- Swiss Re Institute, sigma 1/2026: Natural catastrophes in 2025 (Mar 19, 2026) — $220B economic / $107B insured nat-cat losses; secondary perils a record 92% of insured losses.

- Aon, 2026 Climate and Catastrophe Insight (via Artemis.bm, Jan 20, 2026) — $260B economic / $127B insured 2025 losses; Greg Case on record capital and alternative risk transfer.

- Artemis.bm, catastrophe bond & ILS market data — 2025 record issuance of $25.6B (+45% YoY, 122 deals); ~$65.9B outstanding mid-2026.

- AM Best / Neuberger Berman / Wharton — Trigger mechanics; indemnity structures represent approximately 75% of the market; parametric triggers introduce basis risk.

- California Assembly Insurance Committee, FAIR Plan Oversight (Jan 2026) — Total exposure reached $724B by Dec 2025, a 230% increase from Sep 2024.

- Performance figures: Massive (Polygon-compatible) adjusted daily closes, retrieved Jun 25, 2026.

Disclaimer: The tickers mentioned (AON, MMC, RNR, EG, ILS) are structural expressions of the physical mechanisms described above, not investment recommendations. See our full Disclaimer for details.

Liquidity & size of the names above

Data as of 2026-06-26 · Massive/Polygon, last ~30 trading days · figures move daily

Real figures from market data (2026-06-23 (last ~30 trading days)). Size tiers reflect median daily dollar volume — how easily a position can actually be entered or exited. This is reference data, not a recommendation.

Liquidity, in plain terms: how easily you can get in and out. Deep means you can trade freely without moving the price; Thin means even small orders can move it — mind the spread.

What this does not tell you — valuation. A real structural deficit does not mean the price hasn’t already discounted it. These figures show size and tradeability only; we deliberately do not screen for valuation, solvency, or whether a name is cheap or expensive today. Do your own valuation work.

| Ticker | Name | Type | Market cap | Median daily $ vol | Liquidity |

|---|---|---|---|---|---|

| RNR | RenaissanceRe Holdings Ltd.Bermuda reinsurer with a large third-party ILS capital platform; earns hard-market underwriting margins PLUS capital-light fee income for managing other people's catastrophe capital. The truest single-name expression of the risk-transfer thesis; still two-sided (a major cat year hits book value). | Stock | $13.2B | $98.1M | Liquid |

| AON | Aon plc Class ADominant global broker (incl. reinsurance via Aon Re). Fee/commission model — does NOT hold catastrophe risk; profits from the volume and repricing of risk transfer. Lower-beta adjacency that does best when the market is functioning, not collapsing. | Stock | $69.5B | $509.8M | Deep |

| MMC | Marsh McLennan — insurance/reinsurance brokerWorld's largest insurance broker; reinsurance via Guy Carpenter. Same fee-based, lower-beta intermediary profile as AON; benefits from rising premium volume and ILS issuance flow rather than holding tail risk. | ETF | n/a · ETF | n/a | Unknownthin — mind the spread |

| EG | Everest Group, Ltd.Active reinsurer that benefits from hard-market pricing but carries catastrophe risk more nakedly than RNR (less fee-based ILS buffer). The most two-sided profile here: strong quiet years, painful loss years. | Stock | $13.7B | $131.2M | Deep |

| ILS | Brookmont Catastrophic Bond ETFFirst US-listed, daily-tradable cat-bond ETF (launched Apr 2025). The most direct retail way to BE the capital earning the premium insurers pay to shed tail-risk; low-volatility/bond-like, NOT equity-style upside. Young/small fund — liquidity caveat; NAV would drop sharply if a major insured catastrophe triggers the underlying bonds. | ETF | n/a · ETF | $598.6K | VeryThinthin — mind the spread |

Tiers: Deep ≥ $100M/day · Liquid $20–100M · Moderate $3–20M · Thin $1–3M · < $1M = execution risk. The note under each name is a sourced exposure disclosure (how pure or diluted the play is), not a valuation view. Source: Massive/Polygon aggregates, last ~30 trading days (snapshot 2026-06-26). Figures move daily.

Found this useful? AtomProphet is independent and reader-funded — you can support the research & hosting ↓

Get the next cascade in your inbox

One short email when a new analysis drops — a single constraint traced end to end, from the physics to the chokepoint to the tickers, with the honest bear case kept in view. No marketing, no tracking, no noise.

- One email per published analysis — typically a few a month, never a daily blast

- The full cascade: driver → chokepoint → vetted, live-liquidity tickers

- The counter-case spelled out, not buried

No account, no paywall. Double opt-in, and one-click unsubscribe in every email.

Support the research & hosting

AtomProphet is independent, ad-light, and reader-funded. Contributions help cover data feeds, hosting, and the time behind the Cascade Graph — they keep this research free and open. A tip buys nothing, unlocks nothing, and is not payment for advice or for any security mentioned anywhere on this site.

Bitcoin37h98hpiHz6BW6ELvRLagk7BBo8UUtxeSh USDC · Base 0x1ac1Abe9eCAd5fAd8fF55B188E079b52cD1e6415